2014/06/23

2014/06/19

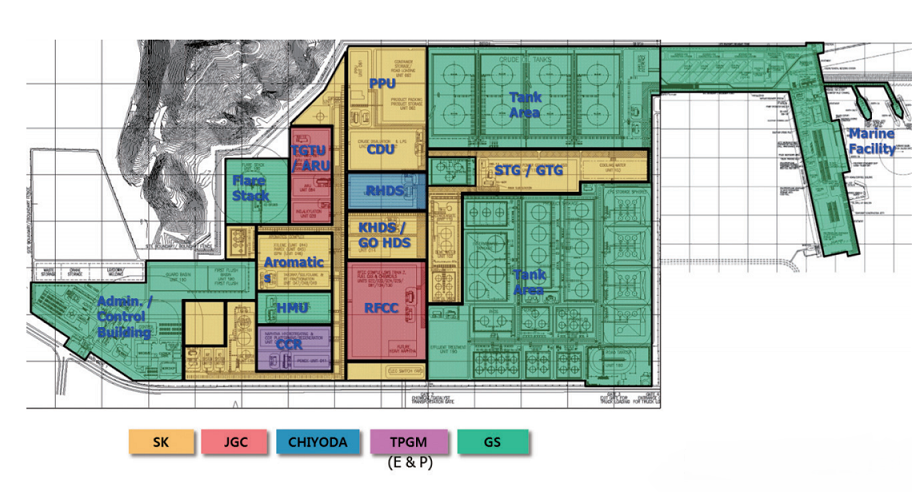

Nghi Son Refinery and Petrochemical LLC (NSRP)

Plan ADD 건축사 사무소 GS건설과 응이손 정유 프로젝트 현지화 설계 및 인허가 컨설팅 계약

PetroVietnam‘s Chairman , Mr Phung Dinh Thuc confirmed during a visit on the site of the Nghi Son refinery project that the preparation work was completed in October 2012 so that the construction could start in 2013.

The Nghi Son Refinery and Petrochemical LLC (NSRP) is a joint venturebetween Vietnam Oil and Gas Group (PetroVietnam), Kuwait Petroleum International (KPI), Idemitsu Kosan Co., Ltd. (Idemitsu), and Mitsui Chemicals Inc. (Mitsui) established in 2008 to build the Vietnam largest refinery and petrochemical complex in Vietnam.

Within the Nghi Son Refinery and Petrochemical joint venture, PetroVietnam and its partners share the working interests:

Within the Nghi Son Refinery and Petrochemical joint venture, PetroVietnam and its partners share the working interests:

- PetroVietnam 30%

- Kuwait Petroleum International 35.1%

- Idemitsu 35.1%

- Mitsui 4.7%

Currently, Vietnam holds only one refinery, theDung Quat refinery, with a capacity of 130,050 b/dcovering only 35% of the domestic market.

The actual consumption of refined products isincreasing in Vietnam by 6 to 8% so that therequired capacity of production in 2020 should reach 600,000 b/d.

In this perspective and after several delays the Nghi Son Refinery project should add 200,000 b/d (10 million t/y) capacity by 2016.

With the petrochemical complex to be integrated in the refinery, the whole Nghi Son refinery andpetrochemical project should require $8 billion capital expenditure.

Foster Wheeler completed FEED on Nghi Son refinery

Located close to the Hai Yen, Mai Lam and Tinh Hai Communes, in the Nghi Son Economic Zone (NSEZ) in the Thanh Hóa Province 215 kilometers south of Hanoi and about 80 km north of Vinh City (Nghe An Province), the Nghi Son Refinery project includes an:

- Onshore part for the refining and petrochemical complex

- Offshore infrastructure for the on and off loading of the vessels

The onshore part of the Nghi Son refinery project will cover 400 ha with 200,000 b/d of crude oil refining capacity to produce:

- 74,000 b/d of Diesel

- 46,000 b/d of Gasoline and LPG

- 12,000 b/d of Kerosen and Jetfuel

- Fuel oil and bitumen

- 400,000 t/y of Polypropylene

- 40,000 t/y of Purified terephthalic acid (PTA)

- 300,000 t/y of Polyethylene terephthalate (PET)

The offshore part of the Nghi Son Refinery project will take 36ha in front of the refinery to integrate:

The offshore part of the Nghi Son Refinery project will take 36ha in front of the refinery to integrate:

- 35 kilometers crude oil import pipeline to connect the single point of mooring (SPM) of the tankers to the refinery

- Two jetties of two berth each to export jet fuel, paraxylene, benzene, gasoline, LPG, sulphur and containerized Polypropylene

- Product export pipelines system to link the refinery and petrochemical tank farms to the jetties

- LPG dedicated export pipeline will supply an LPG tank on the jetty

- Sulfur Forming and Storage unit with handling, weighting and shiploading facilities

Axens will supply the technology for the

- Residue Fluidized Catalytic Cracking (RFCC)

- Prime-D Gas Oil desulfurization unit

- Prime-K Kerozene desulfurization unit

Foster Wheeler completed the front end engineering and design (FEED) and will supply the license for the delayed coker.

The engineering companies should start to work on the engineering, procurement and construction (EPC)contracts on first half 2013 . Plan ADD is converted to work with the currently approved design service design

The Japan Bank for International Cooperation provides 70% of the financing and Kuwait will supply 100% of the crude oil.

With this Nghi Son Refinery and Petrochemical complex project, will PetroVietnam increases its local production of refined products, Kuwait secures export of crude oil, Idemitsu and Mitsui find a unique opportunity of competitive labor costs and feedstock to produce petrochemical products in a region where the market is booming.

탄 호아주 인민위원회 청사에서 열린 이번 계약식에는 최광철 SK건설 사장과 우상룡 GS건설 해외사업총괄(CGO) 사장, 히데토 무라카미 응이손 정유.석유화학회사 대표이사, 베트남 정부인사 등이 참석했다. 응이손 프로젝트는 오는 2017년까지 수도 하노이에서 남쪽으로 200㎞ 떨어진 탄 호아 지역에 하루 평균 20만 배럴의 정유를 정제할 수 있는 베트남 내 최대이자 두 번째 정유.석유화학플랜트를 짓는 공사다. SK건설은 원유정제설비(CDU)와 전기.수처리시설 등 부대시설 공사를 맡아 수행하며 GS건설은 수소 생산설비와 정유 저장설비 등 공사를 수행한다. Plan ADD 건축사 사무소는 현지 인허가와 변환 설계를 맡는다.

SK건설과 GS건설은 지난 27일 베트남 응이손 정유.석유화학회사와 21억달러 규모의 정유·석유화학플랜트 공사 계약(사진)을 체결했다고 28일 밝혔다.

탄 호아주 인민위원회 청사에서 열린 이번 계약식에는 최광철 SK건설 사장과 우상룡 GS건설 해외사업총괄(CGO) 사장, 히데토 무라카미 응이손 정유.석유화학회사 대표이사, 베트남 정부인사 등이 참석했다. 응이손 프로젝트는 오는 2017년까지 수도 하노이에서 남쪽으로 200㎞ 떨어진 탄 호아 지역에 하루 평균 20만 배럴의 정유를 정제할 수 있는 베트남 내 최대이자 두 번째 정유.석유화학플랜트를 짓는 공사다. SK건설은 원유정제설비(CDU)와 전기.수처리시설 등 부대시설 공사를 맡아 수행하며 GS건설은 수소 생산설비와 정유 저장설비 등 공사를 수행한다. Plan ADD 건축사 사무소는 현지 인허가와 변환 설계를 맡는다.

최광철 SK건설 사장(앞줄 오른쪽 첫번째)과 우상룡 GS건설 해외사업총괄 사장(앞줄 오른쪽 두번째), 히데토 무라카미 응이손 정유.석유화학회사 대표이사(앞줄 오른쪽 세번째)가 계약서에 서명하고 있다.

2014/06/18

Về kế toán thuật ngữ Anh-Việt

THUẬT NGỮ KẾ TOÁN ANH - VIỆT

1. Break-even point: Điểm hòa vốn2. Business entity concept: Nguyên tắc doanh nghiệp là một thực thể

3. Business purchase: Mua lại doanh nghiệp

4. Calls in arrear: Vốn gọi trả sau

5. Capital: Vốn

6. Authorized capital: Vốn điều lệ

7. Called-up capital: Vốn đã gọi

8. Capital expenditure: Chi phí đầu tư

9. Invested capital: Vốn đầu tư

10. Issued capital: Vốn phát hành

11. Uncalled capital: Vốn chưa gọi

12. Working capital: Vốn lưu động (hoạt động)

13. Capital redemption reserve: Quỹ dự trữ bồi hoàn vốn cổ phần

14. Carriage: Chi phí vận chuyển

15. Carriage inwards: Chi phí vận chuyển hàng hóa mua

16. Carriage outwards: Chi phí vận chuyển hàng hóa bán

17. Carrying cost: Chi phí bảo tồn hàng lưu kho

18. Cash book: Sổ tiền mặt

19. Cash discounts: Chiết khấu tiền mặt

21. Category method: Phương pháp chủng loại

22. Cheques: Sec (chi phiếú)

23. Clock cards: Thẻ bấm giờ

24. Closing an account: Khóa một tài khoản

25. Closing stock: Tồn kho cuối kỳ

26. Commission errors: Lỗi ghi nhầm tài khoản thanh toán

27. Company accounts: Kế toán công ty

28. Company Act 1985: Luật công ty năm 1985

29. Compensating errors: Lỗi tự triệt tiêu

30. Concepts of accounting: Các nguyên tắc kế toán

31. Conservatism: Nguyên tắc thận trọng

32. Consistency: Nguyên tắc nhất quán

33. Control accounts : Tài khoản kiểm tra

34. Conventions: Quy ước

35. Conversion costs: Chi phí chế biến

36. Cost accumulation: Sự tập hợp chi phí

37. Cost application: Sự phân bổ chi phí

38. Cost concept: Nguyên tắc giá phí lịch sử

39. Cost object: Đối tượng tính giá thành

40. Cost of goods sold: Nguyên giá hàng bán

41. Credit balance: Số dư có

42. Credit note: Giấy báo có

43. Credit transfer: Lệnh chi

44. Creditor: Chủ nợ

45. Cumulative preference shares: Cổ phần ưu đãi có tích lũy

46. Current accounts: Tài khoản vãng lai

47. Current assets: Tài sản lưu động

48. Curent liabilities: Nợ ngắn hạn

49. Current ratio: Hệ số lưu hoạt

50. Debentures: Trái phiếu, giấy nợ

51. Debenture interest: Lãi trái phiếu

52. Debit note: Giấy báo Nợ

53. Debtor: Con nợ

54. Depletion: Sự hao cạn

55. Depreciation: Khấu hao

56. Causes of depreciation: Các nguyên do tính khấu hao

57. Depreciation of goodwill: Khấu hao uy tín

58. Nature of depreciation: Bản chất của khấu hao

59. Provision for depreciation: Dự phòng khấu hao

60. Reducing balance method: Phương pháp giảm dần

61. Straight-line method: Phương pháp đường thẳng

62. Direct costs: Chi phí trực tiếp

63. Directors: Hội đồng quản trị

64. Directors’ remuneration: Thù kim thành viên Hội đồng quản trị

65. Discounts: Chiết khấu

66. Discounts allowed: Chiết khấu bán hàng

67. Cash discounts: Chiết khấu tiền mặt

68. Provision for discounts: Dự phòng chiết khấu

69. Discounts received: Chiết khấu mua hàng

70. Dishonored cheques: Sec bị từ chối

71. Disposal of fixed assets: Thanh lý tài sản cố định

72. Dividends: Cổ tức

73. Double entry rules: Các nguyên tắc bút toán kép

74. Dual aspect concept: Nguyên tắc ảnh hưởng kép

75. Drawing: Rút vốn

76. Equivalent units: Đơn vị tương đương

77. Equivalent unit cost: Giá thành đơn vị tương đương

78. Errors: Sai sót

79. Expenses prepaid: Chi phí trả trước

80. Factory overhead expenses: Chi phí quản lý phân xưởng

81. FIFO (First In First Out): Phương pháp nhập trước xuất trước

82. Final accounts: Báo cáo quyết toán

83. Finished goods: Thành phẩm

84. First call: Lần gọi thứ nhất

85. Fixed assets: Tài sản cố định

86. Fixed capital: Vốn cố định

87. Fixed expenses: Định phí / Chi phí cố định

88. General ledger: Sổ cái

89. General reserve: Quỹ dự trữ chung

90. Going concerns concept: Nguyên tắc hoạt động lâu dài

91. Goods stolen: Hàng bị đánh cắp

92. Goodwill: Uy tín

93. Gross loss: Lỗ gộp

94. Gross profit: Lãi gộp

95. Gross profit percentage: Tỷ suất lãi gộp

96. Historical cost: Giá phí lịch sử

97. Horizontal accounts: Báo cáo quyết toán dạng chữ T

98. Impersonal accounts: Tài khoản phí thanh toán

99. Imprest systems: Chế độ tạm ứng

100. Income tax: Thuế thu nhập

101. Increase in provision: Tăng dự phòng

102. Indirect costs: Chi phí gián tiếp

103. Installation cost: Chi phí lắp đặt, chạy thử

104. Intangible assets: Tài sản vô hình

105. Interpretation of accounts: Phân tích các báo cáo quyết toán

106. Investments: Đầu tư

107. Invoice: Hóa đơn

108. Issue of shares: Phát hành cổ phần

109. Issued share capital:Vốn cổ phần phát hành

110. Job-order cost system: Hệ thống hạch toán chi phí sản xuất theo công việc/ loạt sản phẩm

111. Journal: Nhật ký chung

112. Journal entries: Bút toán nhật ký

113. Liabilities: Công nợ

114. LIFO (Last In First Out): Phương pháp nhập sau xuất trước

115. Limited company: Công ty trách nhiệm hữu hạn

116. Liquidity: Khả năng thanh toán bằng tiền mặt (tính lỏng/ tính thanh khoản)

117. Liquidity ratio: Hệ số khả năng thanh toán

118. Long-term liabilities: Nợ dài hạn

119. Loss: Lỗ

120. Gross loss: Lỗ gộp

121. Net loss: Lỗ ròng

122. Machine hour method: Phương pháp giờ máy

123. Manufacturing account: Tài khoản sản xuất

124. Mark-up: Tỷ suất lãi trên giá vốn

125. Margin: Tỷ suất lãi trên giá bán

126. Matching expenses against revenue: Khế hợp chi phí với thu nhập

127. Materiality: Tính trọng yếu

128. Materials: Nguyên vật liệu

129. Money mesurement concept: Nguyên tắc thước đo bằng tiền

130. Net assets: Tài sản thuần

131. Net book value: Giá trị thuần

132. Net realizable value: Giá trị thuần thực hiện được

133. Nominal accounts: Tài khoản định danh

134. Nominal ledger: Sổ tổng hợp

135. Notes to accounts: Ghi chú của báo cáo quyết toán

136. Objectivity: Tính khách quan

137. Omissions, errors: Lỗi ghi thiếu

138. Opening entries: Các bút toán khởi đầu doanh nghiệp

139. Opening stock: Tồn kho đầu kỳ

140. Operating gains: lợi nhuận trong hoạt động

141. Ordinary shares: Cổ phần thường

142. Original entry, errors : Lỗi phát sinh từ nhật ký

143. Output in equivalent units: Lượng sản phẩm tính theo đơn vị tương đương

144. Overdraft: Nợ thấu chi

145. Overhead application base: Tiêu thức phân bổ chi phí quản lý phân xưởng

146. Overhead application rate: Hệ số phân bổ chi phí quản lý phân xưởng

147. Oversubscription of shares: Đăng ký cổ phần vượt mức

148. Paid-up capital: Vốn đã góp

149. Par, issued at: Phát hành theo mệnh giá

150. Periodic stock: Phương pháp theo dõi tồn kho định kỳ

101. Increase in provision: Tăng dự phòng

102. Indirect costs: Chi phí gián tiếp

103. Installation cost: Chi phí lắp đặt, chạy thử

104. Intangible assets: Tài sản vô hình

105. Interpretation of accounts: Phân tích các báo cáo quyết toán

106. Investments: Đầu tư

107. Invoice: Hóa đơn

108. Issue of shares: Phát hành cổ phần

109. Issued share capital:Vốn cổ phần phát hành

110. Job-order cost system: Hệ thống hạch toán chi phí sản xuất theo công việc/ loạt sản phẩm

111. Journal: Nhật ký chung

112. Journal entries: Bút toán nhật ký

113. Liabilities: Công nợ

114. LIFO (Last In First Out): Phương pháp nhập sau xuất trước

115. Limited company: Công ty trách nhiệm hữu hạn

116. Liquidity: Khả năng thanh toán bằng tiền mặt (tính lỏng/ tính thanh khoản)

117. Liquidity ratio: Hệ số khả năng thanh toán

118. Long-term liabilities: Nợ dài hạn

119. Loss: Lỗ

120. Gross loss: Lỗ gộp

121. Net loss: Lỗ ròng

122. Machine hour method: Phương pháp giờ máy

123. Manufacturing account: Tài khoản sản xuất

124. Mark-up: Tỷ suất lãi trên giá vốn

125. Margin: Tỷ suất lãi trên giá bán

126. Matching expenses against revenue: Khế hợp chi phí với thu nhập

127. Materiality: Tính trọng yếu

128. Materials: Nguyên vật liệu

129. Money mesurement concept: Nguyên tắc thước đo bằng tiền

130. Net assets: Tài sản thuần

131. Net book value: Giá trị thuần

132. Net realizable value: Giá trị thuần thực hiện được

133. Nominal accounts: Tài khoản định danh

134. Nominal ledger: Sổ tổng hợp

135. Notes to accounts: Ghi chú của báo cáo quyết toán

136. Objectivity: Tính khách quan

137. Omissions, errors: Lỗi ghi thiếu

138. Opening entries: Các bút toán khởi đầu doanh nghiệp

139. Opening stock: Tồn kho đầu kỳ

140. Operating gains: lợi nhuận trong hoạt động

141. Ordinary shares: Cổ phần thường

142. Original entry, errors : Lỗi phát sinh từ nhật ký

143. Output in equivalent units: Lượng sản phẩm tính theo đơn vị tương đương

144. Overdraft: Nợ thấu chi

145. Overhead application base: Tiêu thức phân bổ chi phí quản lý phân xưởng

146. Overhead application rate: Hệ số phân bổ chi phí quản lý phân xưởng

147. Oversubscription of shares: Đăng ký cổ phần vượt mức

148. Paid-up capital: Vốn đã góp

149. Par, issued at: Phát hành theo mệnh giá

150. Periodic stock: Phương pháp theo dõi tồn kho định kỳ

151. Perpetual stock: Phương pháp theo dõi tồn kho liên tục

152. Personal accounts: Tài khoản thanh toán

153. Petty cash books: Sổ quỹ tạp phí

154. Petty cashier: Thủ quỹ tạp phí

155. Physical deteration: Sự hao mòn vật chất

156. Physical units: Đơn vị (sản phẩm thực tế)

157. Posting: Vào sổ tài khoản

158. Predetermined application rate: Hệ số phân bổ chi phí định trước

159. Preference shares: Cổ phần ưu đãi

160. Cummulative preference share: Cổ phần ưu đãi có tích lũy

161. Non-cummulative preference share: Cổ phần ưu đãi không tích lũy

162. Preliminary expenses: Chi phí khởi lập

163. Prepaid expenses: Chi phí trả trước

164. Private company: Công ty tư nhân

165. Profitability: Khả năng sinh lời

166. Prime cost: Giá thành cơ bản

167. Principle, error of: Lỗi định khoản

168. Process cost system: Hệ thống hạch toán CPSX theo giai đoạn công nghệ

169. Product cost: Giá thành sản phẩm

170. Production cost: Chi phí sản xuất

171. Profits: lợi nhuận, lãi

172. Appropriation of profit: Phân phối lợi nhuận

173. Gross profit: Lãi gộp

174. Net profit: Lãi ròng

Subscribe to:

Posts

(

Atom

)